“All truth passes through three stages. First, it is ridiculed. Second, it is violently opposed. Third, it is accepted as being self-evident.” Arthur Schopenhauer

We are currently living the 10th year of the so-called global recovery, after the Great Financial Crisis (GFC) of 2008. We have been “blessed” with Central Bank´s zero (and sometimes negative) interest rate policy for many years and this has definitely numbed the senses of many fund managers.

I would argue not only that most of them have never seen a crash in their lives, but also that some have never seen two or three decent corrections. So, the mere suggestion of a correction is seen as a great buying opportunity, well-known in the financial markets as “buy the dip”. Followers of this movement have been able to deliver solid results, as every dip has proven to be a real buying opportunity.

This kind of movement works until the day it does not. Suddenly lots of people who have never experienced a bear market are faced with huge (and increasing) losses in their portfolios, as they perceive the “dip” as another great buying opportunity and load up their portfolios with pricey assets at the wrong time.

In any case, this buying opportunity every time there is a “dip” in the markets is becoming very risky.

Now there is something new and very well advertised, but people still are not paying attention. This change, which has been occurring in the recent past, means trouble. The US Central Bank, also known as the “FED”, has started to raise rates and decrease the size of its balance sheet, a movement baptized Quantitative Tightening, or simple, QT.

If the opposite, known as Quantitative Easing, or QE, was responsible for rising share prices, low bond yields, the end of volatility, falling interest rates and increase level of risk appetite, it would be unwise to expect the status quo to remain as it is, as QE transforms into QT.

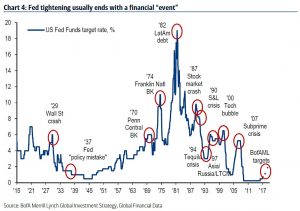

As I mentioned above, most managers have never experienced a crash in their lives, but it is important to remind everyone that all major crashes in the last decades have occurred when the FED was raising rates – I believe this might be the case again.

The chart above shows that every major crash happened when the FED was raising rates. It is unlikely that this time will be different. Actually, as none of the previous problems were actually solved, only brushed under the carpet, it is more likely that this time the complications will be more problematic.

This time things will be different somehow. In 2000 there was a massive internet (private) bubble, which was then rescued after the crash and transformed into a massive property / bank crisis (still private, but less so). This time it is a government problem, as governments and Central Banks have leveraged up their balance sheets to rescue banks.

Now, what might happen if there is another crash in the markets? Well, in my opinion, the Central Banks will do what they always done: come to the rescue. As the saying goes, if all you have is a hammer, everything looks like a nail. So they would most likely reduce interest rates again and might even bring them to a negative territory (in some countries rates are already negative).

And this will bring us to our theme of this month´s newsletter: gold.

I believe gold will immensely benefit from another crisis. I am not cheering for a crisis, but I am just alert to the state of the financial markets around the world. And potential crisis is not on the shortage currently. There is a huge derivatives book from Deutsche Bank which, according to the IMF, is the biggest threat to the financial markets, plus Spanish and Italian banks which are undercapitalized and facing dire straits, to name a few. Italy and India themselves are said to be on the brink of another crisis.

There is also Brexit, whose effects have not yet been seen (if they ever will), renewed tensions between Russia, Iran and the US, bubbles in the Chinese market including banks and properties, property booms beyond understanding in Canada and Australia and conflicts in Syria, Yemen, Saudi Arabia, China´s South Sea and Ukraine.

Rising default rates, significant flattening of the yield curve and increase in the level of debt, both public and private, do not sound like a safe environment.

To top it off, we have the second biggest market valuation in the US in many metrics, leaving even 1929 in the rear view mirror. Below we can see the Shiller PE, a price-earnings ratio based on average inflation-adjusted earnings from the previous 10 years – and, as earnings are susceptible to manipulation (with companies using many tricks, the most obvious being companies issuing cheap debt to buy back shares and increase earnings), this ratio, in my opinion, should be even higher.

As mentioned, this market has been supported by very low (if not negative) nominal rates and lots of money-printing (QEs), which gave incentives for companies to issue debt (bonds) and buyback stocks, decreasing or maintaining its P/E (price/earnings) and, hence, generating a virtuous cycle for management.

This movement has been going on for many years now, and gained a lifeline this year with the Trump repatriation tax on corporates. But, as we know, all good things must come to an end. And this is too much of a good thing.

Keeping markets inflated by printing money is never a sustainable thing. I suspect the smart money is starting to sell and many experienced fund managers, including me, are recommending a strong risk reduction in one´s portfolios.

I see Jeff Gundlach, Stanley Druckenmiller, Paul Singer, Paul Tudor Jones, Bill Gross, George Soros amongst others warning of too many risks ahead, but the markets march undeterred. When knowledgeable and proven fund managers like them start to sound the alarm, one had better take heed. Whilst the young ones are taking every single opportunity to “buy the dip”, the “old” ones are reducing risk. Seems about right.

Do you want a hint that we are due for a serious correction in the markets? I leave you with Janet Yellen, ex-FED chair: ““Would I say there will never, ever be another financial crisis? You know probably that would be going too far but I do think we’re much safer and I hope that it will not be in our lifetimes and I don’t believe it will be.” Well, so much for a prediction. Her predecessors tried to do the same and it ended in disaster.

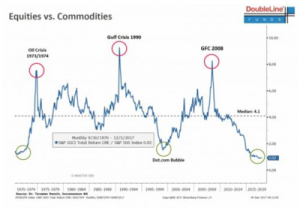

So, what to do? Which kind of asset might benefit from turbulence and risks ahead? Well, certain commodities come to mind and gold shines as a safe haven in these times. I still prefer the uranium space, of which I will write more about in the next article. But commodities in general pose an interesting risk x return relationship for investors, as one can see from the chart below.

I like to buy things when they are inexpensive, and the chart above shows us that commodities might just be the ones to look at. I believe the prospects for gold are looking good from now until the end of the year. The “weak” season for owning gold goes from February until July. July is when the “strong” season to own gold starts, with the Indian harvest and their weddings, Christmas in the Western Hemisphere and the Chinese New Year.

Gold was able to “hold the ground” somehow this year despite a strong US dollar, and the US dollar might not be too strong from now on. I do not like to make predictions about currencies, but since the formation of the FED, in 1913, gold has gone up from US$20 all the way to US$1,250 currently. You can also look at it differently, like the US dollar went down compared to gold.

Some potential good news for gold buying might emerge soon. Elections in the US and the uncertainty in the scenario, threats of retaliation against Trump´s trade wars and negative trade meetings with the Chinese are on the radar, and they might be a headwind for the US dollar.

Besides, Trump wants a weak US dollar. Days before the inauguration, Trump declared that the US dollar was too strong. According to David Woo, head of global rates and foreign exchange research from Bank of America Merrill Lynch, “There’s no question that the Trump administration would not want a strong dollar. A strong dollar does nothing good for whatever Trump is basically trying to do”.

So, the investment in gold is one that has the characteristics that I am looking for at this time: an unappreciated asset, at the cusp of a bull market, under owned, which works as a safe haven in times of trouble (and we are now in trouble season) and entering into the strong phase of the year.

There are many ways to participate in the gold bull run that I believe is coming. One can buy gold itself, some ETFs, a gold fund or many of the listed stocks. But I would like to talk about a gold exploration company today. There are a few that I follow and like, but there might be a short term opportunity here.

I believe exploration companies, with all the risks they bring along, present the highest chance of price increase in the whole gold universe. One can play safe and buy the big names in the sector (which I did, by the way), like Agnico Eagle Mines, Goldcorp, etc, but I believe I found a speculative stock in the sector that deserves some attention.

Investing in exploration companies is not, as most people think, a capital intensive business. Exploration companies can be easily compared to software companies, where people are what really matters.

Investing in good people, with a solid track record, a history of delivering results is normally what works in this sector. I would argue that investing in people in this sector is way more important than investing on a project. So, before I look into the project, I look at the people involved.

Good people have better access to good projects, better access to finance when needed and they are capable of attracting other good people to join the company. They reduce the risks of investing and could increase returns.

Our journey starts in June 2000, with the foundation of ReLODe Ltd, listed on the Australia Stock Exchange (ASX) the next year and later re-baptized Integra Mining (including a change of management, when Chris Cairns became the Managing Director). The company, based in Perth, was specialized in the exploration and production of gold.

After a few years with successful work to increase its reserves (through acquisitions, joint ventures and strategic alliances), the company was finally able to start the extraction of gold in its Randalls Project.

The Randalls Project, commissioned in February 2011, was built on-time and under-budget, two characteristics that are very rare in this business and brought positive attention to management.

By June 2012, Integra had 1.9 million tons of ore at 1.5g/t gold (in today´s value, something around US$120 million).

Integra Mining had a very strong track record of discoveries, as proven by the Salt Creek in 2007, Majestic in 2010 and Imperial in 2011.

The company was well-managed, has little debt and was profitable. Chris Cairns led the company all the way, from 2004 until 2013.

In 2013, Integra was taken over by Silver Lake Resources, another listed gold exploration and producer, for a 40% premium, a nice return for shareholders. The pro-forma combined venture occupied the 5th largest position in listed Australian gold producers, with a market cap of A$1.26 billion.

So, why am I talking about Integra Mining and what is really my investment idea? Well, I talked about Integra Mining because I am looking at another interesting opportunity, in which I believe the returns can be outstanding: Stavely Minerals, a company led now by (drum roll please…) Chris Cairns.

The company did its IPO in 2014, raising $6.1 million. As per their website, Stavely Minerals is a gold exploration company formed to acquire early to advanced stage exploration projects with demonstrated high potential for additional discovery.

The senior team is pretty much the same as that of Integra so, judging by the experience and level of success of management in the previous company, I believe that there might be the case – again.

Stavely Minerals has more than $7million in cash and it´s spending rate is around $500,000/month. This cash should last for approximately another year, but I believe a good opportunity is just around the corner. One does not need to wait for one year, in my opinion.

Management is committed to the project and own circa 34% of the company. It is always reassuring to see this. One of the key things for us is to see alignment of shareholders and management. If management owns a significant part of the company, they will be more interested in its success. Besides, some great resource investors in Australia are also buying into this project.

Stavely Minerals had 2 projects initially, the Stavely and Ararat Projects. They are both in Victoria, a location not very famous for supporting gold mines, but the projects are in areas that I believe could be explored further. The Victorian projects are prospective for copper-gold and some base metals-gold mineralisation.

In 2016, Stavely Minerals acquired the Ravenswood Project, a highly prospective gold-copper exploration in Queensland. This project is prospective for copper-molybdenum-gold.

With this Queensland acquisition and an experienced management team, I believe Stavely Minerals is able to mitigate some of the risks of doing business in Victoria.

In order to preserve cash, management has outsourced most of the investment and is paying the contractors half in cash and half in shares of the company. There is an advantage of paying contractors this way: with the cash, contractors can pay their employees, fuel and other expenses that they incur in their day to day. With the shares, Stavely is able to preserve cash and the contractors are able to benefit from a discovery. The shares that were allocated to contractors have not been sold so far, which shows confidence from the contractors in Stavely Minerals. Besides, there is no pressure on the shares in the stock market.

I am very excited about the prospects for the company, but I would like to focus on the one that I believe is very close to becoming an important discovery, the Thursday´s Gossan Porphyry, in the Stavely Volcanic Belt. It is being drilled as I write, at a pace of 2 holes per month.

The area is a farmland, and the farmer is keen on having the drills there. Obviously, he has been taken care of by the company. Neighbours are already talking and also showed interest in drillings in their areas too. So, one of the big risks for the company is being mitigated, to say the least.

This area is close to the Yarram Park, but not too close. This is a plus when it comes to the approvals and licences.

So, I believe Stavely Minerals is into something there. They have been drilling in one direction and the prospects are looking better than ever. Recent results have intercepted magnetite veins, which could be an indicator to mineralisation. There has been more than 100m intercept of classic porphyry “M” veins (picture below), typical of gold-rich porphyries:

Their drilling demonstrates that they are at the top of the porphyry system, because of the large amounts of veining and the oxidized fluids (the more oxidized the minerals, the greater the probability of having gold and copper).

Everything indicates that they are drilling in the right direction (towards the South-West), where the chances of potential discovery are increasing dramatically. The risk I see on the discovery is a significant structural dislocation of the mineralisation.

I met with the company and I believe this risk is low – obviously, the risk is low for a gold exploration company – as an investment, the risk is quite high. They are drilling in the right direction and they could announce a discovery before the end of the year. I also believe that if they announce a discovery, it is not going to be a little one. This could change the size of the company significantly.

The Stavely Minerals team have done it before and they might be able to do it again. As I mentioned in the beginning, an experienced team who has been successful before is extremely valuable in this area.

I have bought a small speculative position in the company, for less than A$0.30 (it´s A$0.275 as I write). I believe that if a discovery is made in the Thursday´s Gossan Porphyry, something that I believe is quite likely, share prices could go up substantially. In addition, there are a few more projects in this area, like the Toora West, Mount Stavely, Drysdale and Junction. On top of that, there are still projects in Queensland. So, there is optionality, in case a discovery is not made in the next few months in this area.

Disclosure: I have a position in some of the stocks mentioned above but this is not a recommendation and should not be acted upon.